The idea of flexible space has been gaining momentum over the past several years, but in 2018 we saw a profound shift. Last year, the amount of flexible space in Manhattan alone surged to 13.5 million square feet, up from 9.4 million square feet in 2017, according to CBRE research.

Mainly, enterprise companies are starting to embrace flexible space. Why? For decades now, corporations have been looking for ways to make their real estate costs variable in order to swiftly adapt to business fluctuations in the same way that manufacturing, research, and distribution departments have done. And it makes sense. Flexible workspaces allow businesses to leverage real estate as an agile rather than a fixed asset. With agile real estate, you can choose what initial capital expenditure will go into the space, and which contraction and expansion rights you can leverage to align with your business needs.

Let’s zero in on the financial decisions that companies make when they decide between a traditional lease or an agile space.

Agile real estate 1.0: re-thinking the traditional

When does it make sense to use a flexible workspace over a traditional lease? The vast majority of decision-makers at enterprise-level companies think about real estate in terms of capital expenditure.

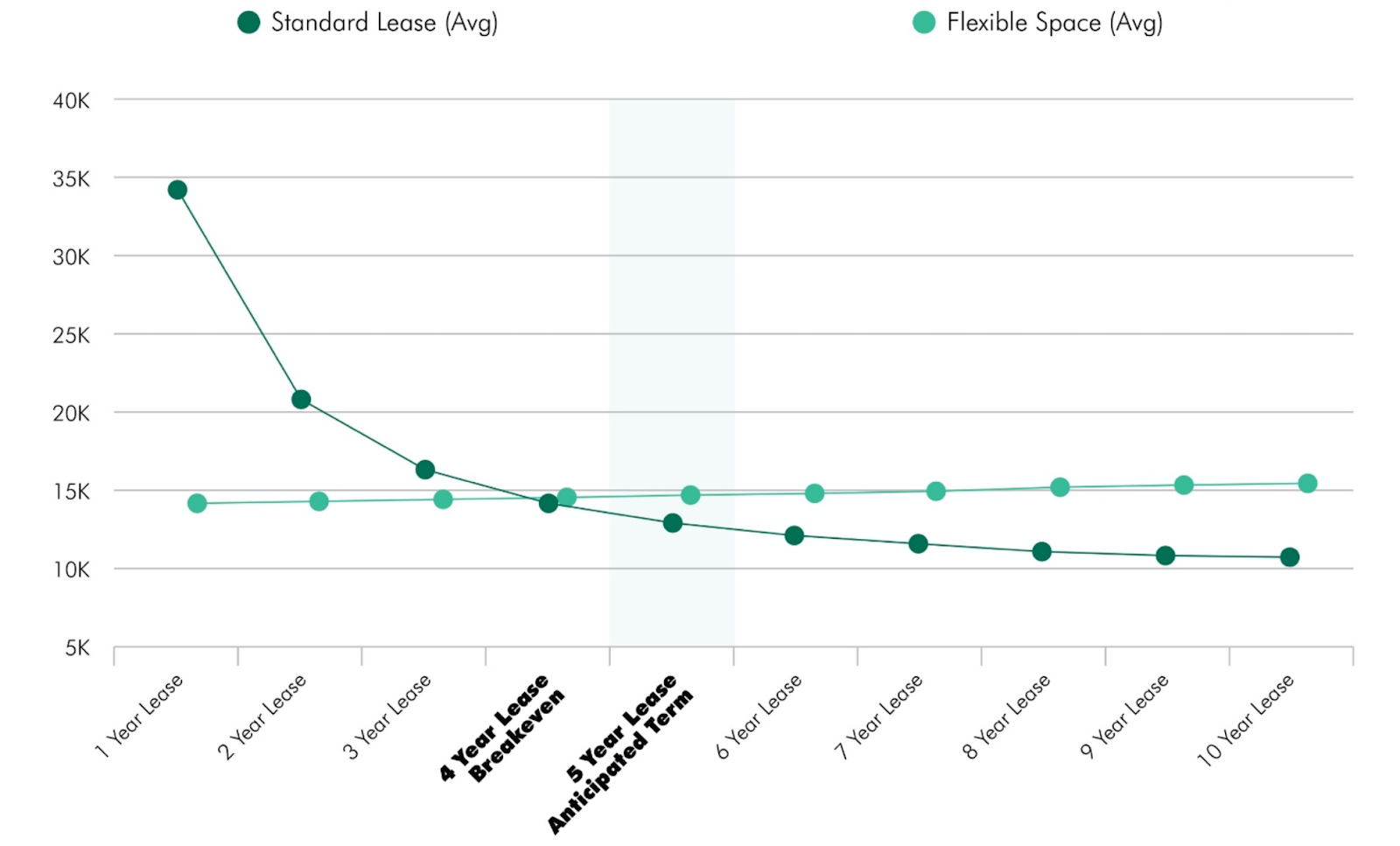

The dark green line represents the costs over time in a standard lease. Because you have the large upfront expenditure of renovating and setting up the building, there’s a high initial cost. This is spread out over time the longer you’re in a space and is therefore an incentive to sign a longer traditional lease.

The lighter green line represents costs per year in a flexible lease, where building and operational costs are baked into the overall cost. This stays relatively flat throughout the years. You can see that at around year four, the two lines converge, and it becomes relatively more expensive to be in a flexible space.

The crystal ball challenge

The problem with this model is that it assumes you can predict the future and that the number of employees will be constant.

These are realities that are, of course, impossible to predict. To this point, CBRE clients tell us that although they may be confident in the overall direction of their business, they could be off on the details by 10 percent to 25 percent depending on unforeseen factors such as the volatility of the market, of their industry, and of the impact of technology on their business.

Introducing uncertainty and risk from the real world into this model changes everything.

Agile real estate 2.0: the true value of flexibility

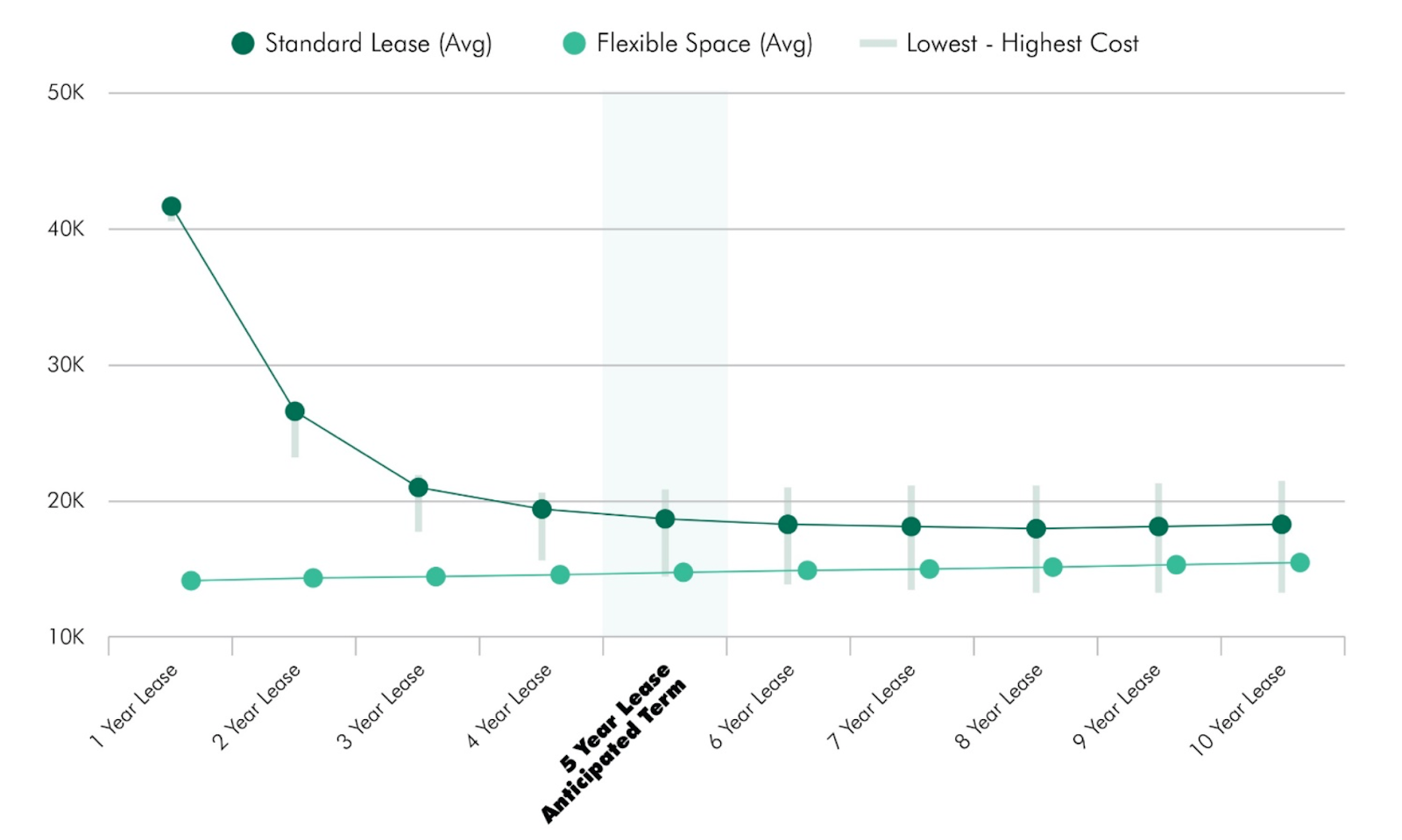

Now, let’s apply the real world to this financial model to include the risk companies encounter over time.

In this case, instead of assuming 100 employees will hold steady or rise at a fixed rate, this model is closer to reality; the number may, in fact, increase to 150 or decrease to 70 in five years.

We call this instance Agile 2.0. By introducing uncertainty, you can see that the two lines illustrating standard and flexible space costs don’t, in fact, converge.

What we’ve found is that the value of flexibility is actually greater than the cost of a flexible lease. This is increasingly how companies think about building agility into their real-estate portfolio. It’s a portrait that reflects long-term business realities, not a short-term, fixed solution.

Comparing traditional and flexible terms

As an example, let’s take a look at how this manifests in traditional and flexible term options:

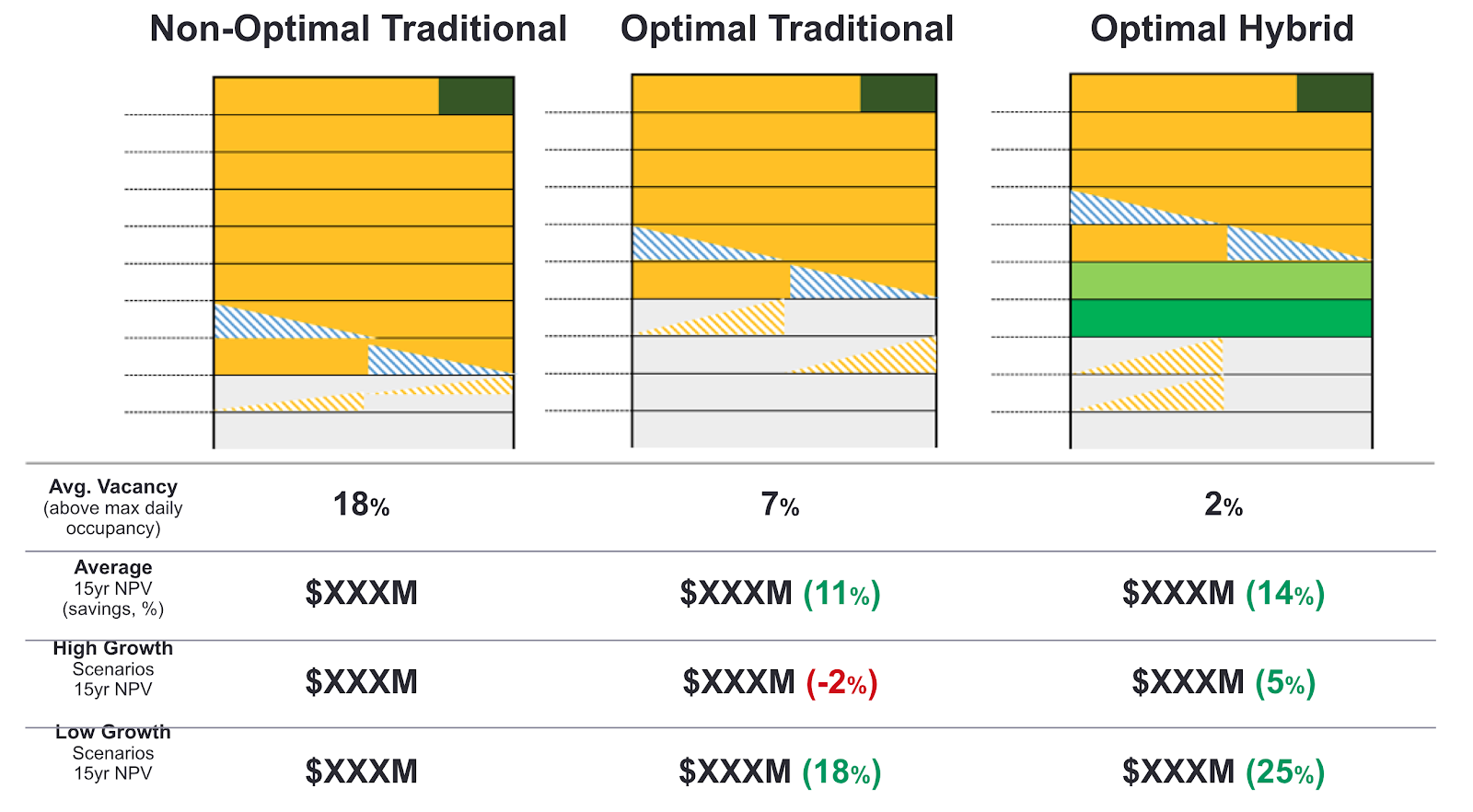

- Non-optimal traditional: In the non-optimal traditional case, the average vacancy rate of this building is 18 percent. Take a look at the yellow block (this scenario assumes the space you’re leasing has a roof deck, represented by the dark green on top). The blue triangle hatch lines represent contraction opportunities for you to give back some space, and the yellow hatch lines represent expansion opportunities if you’d like to expand.

- Optimal traditional: In this model, we introduced more flexibility. Here, you occupy less space and have a few more expansion options. This allows the average vacancy rate to drop to 7 percent, while the average net present value (NPV) is 11 percent lower. In this scenario, if you grow faster than expected, you may be penalized a bit. (Although very fast growth would still be a good problem to have). But if you grow at a slower clip, you’re much more protected against a downside risk. As a whole, flexibility gives you more value.

- Optimal hybrid: Now, let’s look at an optimal hybrid lease. The green bands along the lower floors of the building represent enterprise and traditional coworking spaces. These are spaces that you could grow into but are filled with coworking tenants in the meantime. Under this lease, vacancy drops to just 2 percent and average costs are 14 percent lower. And regardless of whether you have high or low growth, you’ll ultimately have lower costs than with any of the other leases.

The future of agile real estate

Real estate is no longer the static asset it once was. More companies are looking to add agile components to their portfolios, and we only expect that to increase—the data shows that there’s a real economic return with agile real estate.

If you’re looking to get started, think about your business and identify where flexible space could be beneficial. By calculating the impact of potential futures, it’s clear that building flexible workspace into your portfolio will deliver the best return for your business now, and into the future.

To learn more about agile real estate, watch the CBRE and WeWork webinar, “Agility without compromise: secrets of agile real estate.”

WeWork offers companies of all sizes space solutions that help solve their biggest business challenges.

Beth Moore, head of broker development, U.S., Canada, and Israel at WeWork; Brandon Forde, executive managing director, advisory and transaction services at CBRE; and Christelle Bron, senior managing director, advisory and transaction services at CBRE, wrote this article.