- The top 10 U.S. startup metros in this report are: San Francisco, New York, Los Angeles, Boston, Seattle, Austin, Chicago, Washington, D.C., Philadelphia, and San Diego.

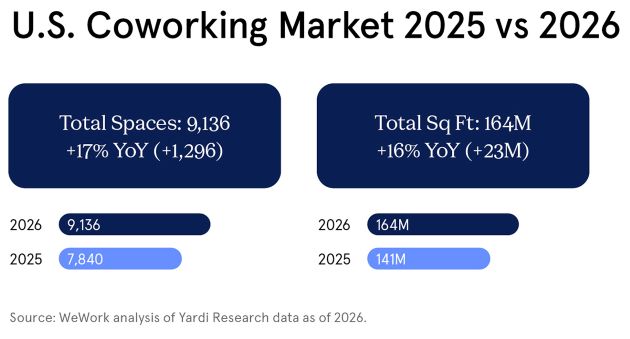

- The U.S. coworking market now exceeds 9,100 locations and 164 million square feet, after growing 17% in a single year.

- All five of the top U.S. startup metros rank within the global top 15.

- New York is the largest coworking market in the country at 753 locations and nearly 20 million square feet, 10% of which was added in the last year alone.

- Philadelphia’s coworking market grew 28% in one year, the fastest rate among the top 10 startup metros.

- 96% of active startups in our locations have maintained or grown their footprint since joining.

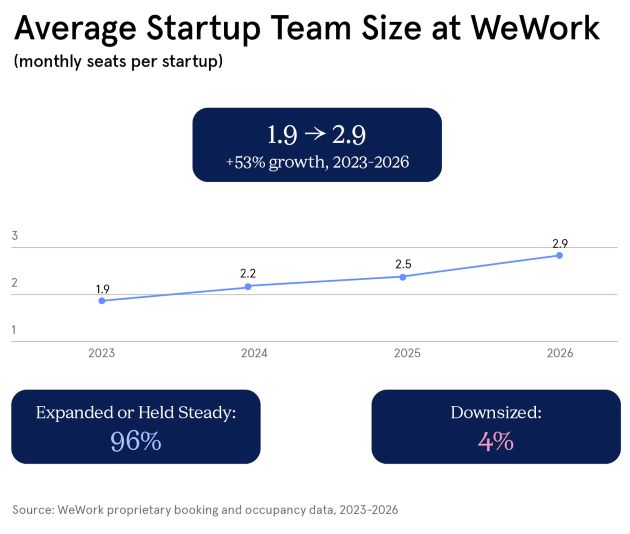

- Average team size among active startups in our portfolio grew by more than half over three years.

The U.S. coworking market grew 17% in a single year, adding nearly 1,300 spaces to reach 9,136 nationwide. That growth wasn’t evenly distributed: it concentrated in the metros where startup activity is strongest; and inside those metros, the small teams choosing flexible workspace are scaling.

What started as an amenity is becoming startup infrastructure.

Here, coworking refers to various forms of flexible workspace, whether that’s an individual membership or space for a team of up to 20. This report focuses on the startups and small businesses using them.

We mapped the link between small business activity and coworking growth across the 20 highest-ranked U.S. startup metros from the 2025 Global Startup Ecosystem Index by StartupBlink, combining it with Yardi Research data on the broader coworking market and WeWork’s own membership and occupancy data. Across WeWork’s 146 U.S. locations, 96% of active startups have either maintained or expanded their footprint since 2023. Average team size has grown more than 50% over three years.

Two years after completing our reorganization, occupancy across our U.S. portfolio is up 4 percentage points year-over-year—with 16-point gains in San Francisco, 13 in Boston, and 33 in San Diego.

The metros seeing the highest increase in occupancy are the same ones leading the country in startup growth.

Startups are behind the wheel of the accelerating U.S. coworking market

Between 2025 and 2026, the U.S. coworking market added 1,296 new spaces, bringing the total to 9,136 locations—a 17% year-over-year increase. Square footage grew at the same rate, adding 23 million square feet to reach 164 million nationwide.

We operate 146 of those locations: 2% of the coworking market by count, but over 5% by square footage, meaning our locations tend to be larger than the market average. That is an important advantage for growing teams: larger spaces give them more room to expand under one roof, without having to change addresses.

The startup picture mirrors the broader market: just as SMBs and startup teams make up 45% of coworking users nationally (DropDesk, 2026), they represent 46% of all members across our U.S. locations. That parallel shaped the question behind this report: how does flexible workspace serve startups and SMBs in the metros where startup activity is strongest, and what does the data tell us about how those small teams are scaling?

96% of active startups have maintained or grown their footprint

Between 2023 and 2026, more than 42,000 startups and small businesses made their first reservation at one of our locations. In a segment where turnover is naturally high, over 9,000 of them are still active as of April 2026, and this group’s footprint is growing: average team size has increased by more than half over the three years. New teams entering our network have consistently started at similar sizes year over year, which means that growth reflects existing companies scaling up, not larger ones joining.

Of those 9,120 active startups and SMBs, 96% have either maintained or expanded their footprint, and just 4% have downsized. Roughly 1 in 12 now operates from multiple WeWork locations. That kind of multi-location presence—once reserved for established companies with the resources to manage multiple leases—is now accessible to teams that are still in their early stages of growth.

Here’s how that pattern plays out across the country’s top 20 startup metros—the top 5 of which rank within StartupBlink’s global 15.

1. San Francisco, CA

The San Francisco metro holds the top spot in StartupBlink’s 2025 ranking, both nationally and globally. Widely considered the world’s startup capital, the metro offers a high concentration of venture capital, proximity to leading global universities, and an ongoing AI boom that keeps drawing talent and companies into the area. That influx needs workspace. The metro added 31 coworking spaces, reaching 228 locations and over 5 million square feet over the past year.

Our 14 locations account for 16% of the metro’s coworking square footage, the highest share of any metro in this study. Roughly 6,100 startups joined us here between 2023 and 2026, and almost a quarter are still active. Average team size increased 56%, and one in ten now operates from more than one of our locations.

2. New York, NY

New York ranks second on StartupBlink’s 2025 index, both nationally and globally, and is the largest coworking market in the country by every measure. The metro has particular depth in fintech, fueled by proximity to Wall Street and a rich investor landscape, and that concentration of new businesses keeps coworking demand high. Over the past year alone, the market added 69 spaces and close to 2 million square feet, bringing the total to 753 locations and nearly 20 million square feet.

Our 30 locations here make up our largest footprint nationally, covering 2.5 million square feet and 13% of the metro’s coworking space. More than 12,000 startups came through our doors between 2023 and 2026. Average team size grew 51%, and 13% of active startups expanded their footprint.

3. Los Angeles, CA

Los Angeles ranks third nationally and fourth globally on the same index. Its coworking demand doesn’t depend on a single industry: where San Francisco runs on AI and New York on fintech, LA spans entertainment tech, aerospace, consumer brands, health tech, and clean energy.

The coworking market supports that diversity-driven growth. The metro added 50 new spaces and just under 1.4 million square feet over the past year, reaching 10 million in total. Across our 17 locations in the metro, more than 6,500 startups signed on between 2023 and 2026. The average team got 48% bigger over that period.

4. Boston, MA

Boston ranks fourth nationally and sixth globally and is the world’s largest biotech hub, powered by one of the highest concentrations of top-tier universities in the country. With AI entering the mix, the region is drawing even more companies to the metro area.

The coworking market follows suit. The metro added 31 spaces over the past year, a 15% increase, reaching 237 locations and close to 6 million square feet. Our 7 buildings welcomed around 1,300 startups between 2023 and 2026. A quarter are still active—the highest retention rate—, with occupancy also jumping 13 percentage points. Teams grew by 40% on average, and one in nine active startups now works from multiple locations in our portfolio.

5. Seattle, WA

Seattle rounds out the national top five and ranks fifteenth globally, built on decades of cloud computing and enterprise software expertise. The coworking market here is more compact—149 locations and 3 million square feet—and grew 7% in locations and 4% in square footage, the slowest in the top five. In a metro this focused, the existing portfolio may simply be well-matched to demand.

We operate 6 buildings covering 291,000 square feet and 10% of the metro’s coworking space. Between 2023 and 2026, nearly 1,500 startups made their first reservation with us. About one in five is still active, and teams have grown 34% on average. Seattle doesn’t produce the flashiest numbers on this list; its strength lies in consistency instead.

The next five: Austin, Chicago, Washington, D.C., Philadelphia, and San Diego

The next five metros on the ranking each bring something unique to the table, and their coworking and startup data reflect that.

Austin (#6 nationally, #16 globally) has been one of the fastest-rising startup ecosystems in the country, powered by favorable government regulation for businesses, lower costs than coastal hubs, and a growing pool of technical talent. The coworking market grew 17% in locations over the past year, above the national rate. We hold 15% of the metro’s coworking square footage here, the second-highest share in this study after San Francisco. Of the roughly 1,450 startups that entered our locations between 2023 and 2026, 15% of those still active have expanded, one of the highest expansion rates on this list.

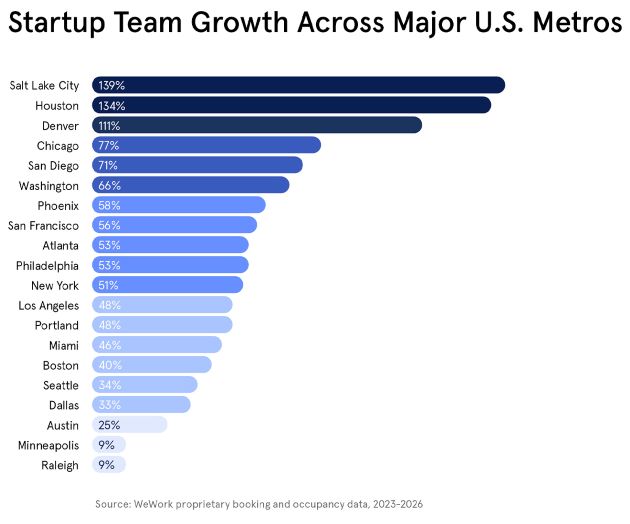

Chicago (#7 nationally, #19 globally) added 53 coworking spaces over the past year, a 19% increase that comfortably outpaced the national rate. The metro’s startup scene tends to fly under the radar, but it has depth in fintech, logistics tech, and B2B SaaS, with a cost of living that gives founders more room to operate. The startup data in our locations stands out: teams here grew by 77% on average, the highest rate of any metro in the top 10.

Washington, D.C. (#8 nationally) is a different kind of startup and SMB market. Govtech, cybersecurity, and defense-adjacent software dominate, which makes sense given the proximity to federal agencies. Coworking growth was the slowest in the top 10 at 7%, reflecting a mature market. But the metro’s smaller ventures in our buildings paint a different picture: they retained members at a higher rate than any other top-10 metro, and teams grew 66%.

Philadelphia (#9 nationally) is where the coworking market is expanding fastest. The metro added 43 spaces over the past year, a 28% jump, the highest growth rate in the entire top 10. The startup ecosystem benefits from direct access to both New York and D.C. along the I-95 corridor and growing strength in industries like health tech and life sciences. Among startups at WeWork’s locations here, average team size grew 53%.

San Diego (#10 nationally) rounds out the top 10 with a dramatic turnaround in the dataset. Occupancy at our locations jumped 33 percentage points, the largest gain of any metro in this study, and teams grew 71%, with 18% of active startups expanding into additional WeWork locations—the highest expansion rate in the top 10. Nearly 2,000 life science companies call the region home, and coworking square footage grew 18% over the past year to support them.

Beyond the top 10: four metros worth watching

The remaining metros in the top 20 each have their own dynamics, but four of them posted numbers that deserve a closer look.

Dallas–Fort Worth (#11) led the country in coworking square footage growth at 29%, adding over 1.4 million square feet in a single year. The metro has been a top destination for corporate relocations for years, and the coworking market is growing to match.

Denver (#14) posted our strongest performance outside the top 10. Teams grew 111%, the highest figure in the dataset after Salt Lake City. Occupancy climbed 12 percentage points, and 17% of active teams now operate from multiple locations, the highest multi-location rate among all metros in this study. Denver’s growing tech scene and lower costs compared to the coasts continue to attract founders, and the data suggests their teams are scaling once they arrive.

Salt Lake City (#15) is the only metro where total coworking square footage declined (-9%). This drop speaks to a broader trend: operators have moved from rapid post-pandemic expansion to optimizing or even downsizing their existing footprint, in favor of smaller, high-demand flex spaces. At the same time, within our single location, team sizes have grown by 2.4 times, the highest rate of any metro in the study. While the sample size is small, it suggests that even inside a market that’s still adjusting, the teams that stay are growing.

Houston (#18) also operates a single location in our portfolio, running at 89% occupancy after a 60-percentage-point jump—the largest occupancy gain in the entire dataset. Teams there grew 134%. As the metro’s economy expands beyond energy into health tech and aerospace, more small businesses crop up, and flex spaces are where many of them get started.

Same trend, different metros

The pattern across these 20 metros is consistent: coworking is growing in the places where startups and small businesses are most active. The teams choosing these spaces are sticking around and, in many cases, expanding. The specifics vary by city: San Francisco leads in operator concentration, New York in sheer volume, Chicago in team growth, San Diego in occupancy recovery. But the common thread is hard to miss.

Flexible workspace may have started as a convenience, but in the metros that matter most for innovation, it’s become the infrastructure that growing businesses rely on.

Click here to download the report.

Methodology

WeWork is a leading global real estate platform that empowers businesses to thrive through world-class flexible workplace solutions, innovative technology services, and hospitality-driven experiences. With a curated portfolio of nearly 600 thoughtfully designed locations worldwide, spanning 45M square feet, WeWork helps more than half a million members—from emerging startups to Fortune 100 companies—achieve their best work.

- For this study, we identified the top 20 U.S. metropolitan areas for startups based on the 2025 Global Startup Ecosystem Index by StartupBlink. As the index ranks urban concentrations rather than metropolitan areas directly, we matched all 1,450 ranked areas to their corresponding U.S. metro and summed the scores of all urban concentrations within each metro to produce a composite ranking.

- For national and metro-level data on the coworking industry, we used proprietary Yardi Research data to determine the number of coworking spaces per metro area, as well as total square footage.

- For this study, coworking refers to flexible workspace solutions across our U.S. locations, including All Access and On-Demand memberships.

- Data for our locations, square footage, and occupancy is proprietary and sourced internally.

- For this study, a startup is defined as a non-enterprise company, characterized by a small initial team size with 20 or fewer seats at first reservation across our U.S. locations (excluding franchises), and includes memberships such as Physical, All Access Basic, All Access Plus, and All Access Pay-As-You-Go. The time scope covers first reservations and activity data from January 1, 2023, through April 2026.

- Startups in this study span a wide range of industries: AI and enterprise software, financial services and fintech, legal services and legal tech, HR and recruiting, advertising and creative agencies, biotech and medical devices, health and wellness, and more.

- Startups, as defined above, account for 99% of all small- and midsize-business (SMB) activity within the respective time scope in our locations, so the study treats the two as effectively interchangeable.